Multivariate Normal Distribution: Theory and Applications

Overview

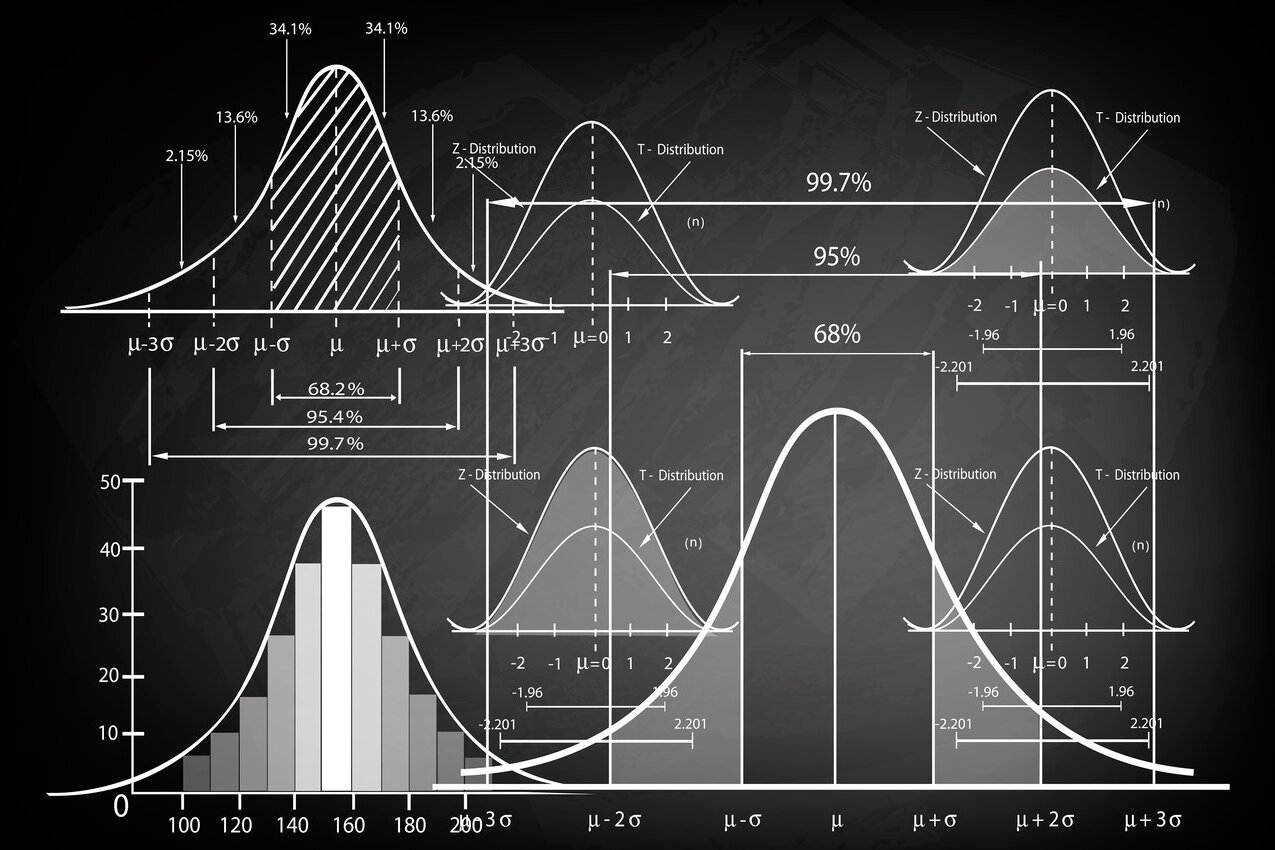

The multivariate normal (MV-N) distribution is a powerful tool in multivariate statistics, providing a generalization of the one-dimensional normal distribution to higher dimensions. The “standard” MV-N distribution, which is its simplest form, describes the joint distribution of a random vector whose entries are mutually independent univariate normal random variables, each with zero mean and unit variance. The general form of the MV-N distribution describes the joint distribution of a random vector that can be represented as a linear transformation of a standard MV-N vector. This distribution has a wide range of applications in statistical inference, including hypothesis testing, estimation, and prediction (Taboga).

Head over to my Github repository!

Sources